In Household Demand and Household Labor Supply we showed how households decide what to spend their income on currently.

Households can also choose to:

- Use present income to finance future spending (Save)

- Use future income to finance current spending (Borrow)

- We can also use present income to enhance future production possibilities (investing)

Borrowing

Most people cannot finance large purchases like a house or car using current income and savings. When you borrow, you finance current purchases with future income. Most of the time you will pay a fee to the lender for the use of his money. The fee is usually in the form of interest.

Saving

When you save, you use current income to finance future spending. When we save, we usually put our money in something that can generate an income. There are lots of options available on financial markets. Examples are:

- Saving accounts

- Money Market funds

- Stocks (Called shares in South Africa)

- Corporate Bonds

When you put your money in financial markets, you are actually lending it out and the borrower pays you a fee for its use.

Interest

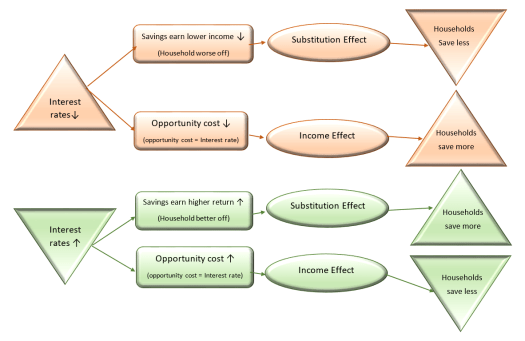

Just like changes in wages affect household behavior, changes in interest rates also affect households behavior in financial markets. When interest rates are higher, borrowing is more expensive, and you will earn a higher return on your savings.

Will people save more if the interest rates are higher? Just like with wages, the answer is not so clear.

Empirical evidence shows that people save more when interest rates are high. The substitution effect is stronger than the income effect.

It is important to know that the money households save is mostly used by businesses to produce or invest in their businesses. Over the long term, capital investments in businesses is constraint by the savings rate of households. Which also means that economic growth is constraint by the savings rate of households.

The more we save, the better the economy could grow and the better off we will all be.

References

Karl E. Case, Ray C.Fair, Principles of economics. Seventh Edition, Pearson Prentice Hall, 2004, Chapter 5

2 Replies to “Saving and Borrowing”