Households choose products and services based on:

- The prices of the products/services as well as prices of substitutes and compliments.

- The household income and accumulated wealth

- Tastes and preferences

- Household’s expectations about the future.

The set of options available to us are limited by income, wealth and prices (the first two items on the list). We refer to this as the budget constraint.

Tastes/preferences and expectations about the future (the last two items on the list) determines what option the household will choose from the set of available options.

Budget constraints

Say for example I earn R 10 000 per month and I am looking for a place to rent. I evaluated 4 options.

Option D will not work, because it does not fall within my budget. My available options are A, B and C. I will choose between them by looking at my tastes and preferences. If a nice big apartment is more important to me than extra money for food and other expenses, I may choose option C. But if I love going out and eating at expensive restaurants, option A may be better for me.

So when a household choose between available options they are weighing the product/service against all other products/services they could buy with the same money.

This brings me to the concept of opportunity cost

Opportunity cost

The real value of a product or service is the value of other products or services you could buy with the same money. Opportunity cost is the best alternative we give up when we make a choice.

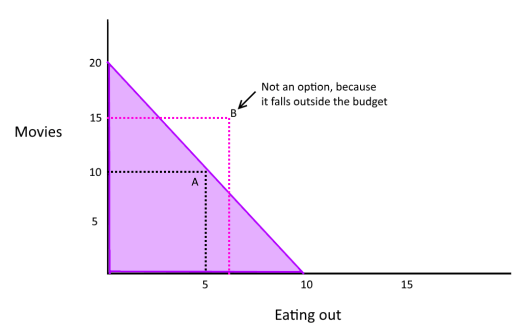

To Illustrate this, lets say you spend money on only two things, eating out or going to the movies. For R 2000 you can eat out 10 times, or you can go to the movies 20 times. The purple area in the graph represents the possible combinations from which you can choose to spend your R 2000. Every time you eat out, you sacrifice movies. And every time you go to the movies, you sacrifice eating out.

B is not an option, because it falls outside your budget.

On a personal note… next time we see something we want to buy, we must take a moment to think what we are sacrificing in the process. We sometimes buy things in the heat of the moment, only to realize later what we should have bought instead.

Utility is closely related to the concept of opportunity cost.

Utility

Utility is the satisfaction we get from one product relative to another. When we evaluate our options, we basically choose which option will give us the most satisfaction.

The law of diminishing marginal utility

Most people will allocate their income across different products and services. The reason why they prefer variety is because of diminishing marginal utility. Marginal utility is the additional satisfaction you get from consuming one more unit of something. To explain this, think of the best movie you ever watched. The first time you watched, it was awesome. The second time was still cool, but the excitement diminished slightly. After watching the movie ten more times, you will probably start looking for something better to do.

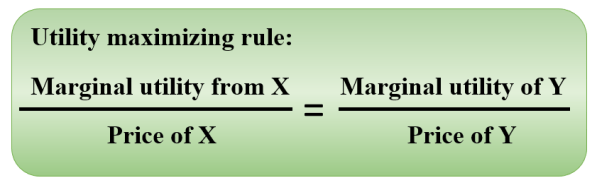

Utility maximizing rule

Like they say, variety is the spice of life. A consumer will keep on spreading out his expenditure until he reach maximum marginal utility. Maximum marginal utility is that point where the marginal utility of product X divided by it’s price is equal to the marginal utility of product Y divided by its price.

The Income effect

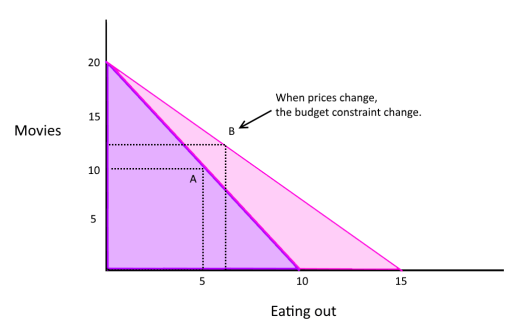

We said the set of available options is determined by prices, income and wealth… the budget constraint.

A change in the price of one product does not change only the quantity demanded for that product. It changes the whole opportunity set which also affects the quantity demanded for other products.

Let’s say in our example the price of food drops and eating out becomes more affordable. We can now eat out 15 times instead of 10. This expands the whole opportunity set. We can now eat out more and watch more movies (or keep the cash and save).

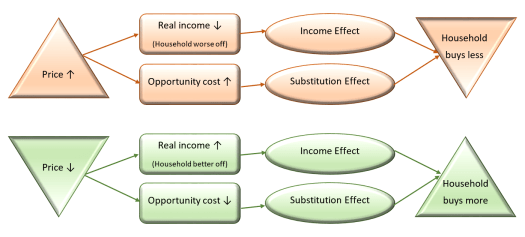

If the price of something we buy falls, we are better off. We can now buy more of that product or something else. When the price of something we buy increase, we are worse off.

The Substitution Effect

When the price of a product falls so that it now becomes cheaper relative to other products, people may substitute products they use with the cheaper product. Likewise, when a price increase so that it now becomes more expensive relative to other products, people will start to diversify away from the more expensive product.

Consumer surplus

The true cost of an item is the value of those things you sacrifice when you buy the item. Consumer surplus is when the value a product has to you is more than the market price. In other words, you pay less for it than the maximum you would be willing to pay. Consumer surplus measurement should be a key element in the cost-benefit analysis of any public project

The Diamond/Water paradox

The price of a product, often does not reflect the value in use. A good example is the difference between water and diamonds. Water is really cheap but very useful. Diamonds on the other hand, are not so useful but really expensive. The reason is that water is in plentiful supply, while diamonds are not. We can enjoy water at a huge consumer surplus. If water was completely free, there would still be a limit to how much water we could use. If water was scarce it would be really expensive.

Up until now we assumed a fixed income to simplify the explanation of consumer demand. Let’s look at the decisions that affect the income of households.

References

Karl E. Case, Ray C.Fair, Principles of economics. Seventh Edition, Pearson Prentice Hall, 2004, Chapter 5

6 Replies to “Household Demand”